Interest rates in the US have been close to zero since the depths of the financial crisis but global investors are braced for change, as the country’s central bank prepares to raise borrowing costs. The first in an expected string of small increases could come as soon this week, with the Federal Reserve rate-setting committee starting a two-day meeting on Wednesday where it will consider a rise. The ramifications of the decision, announced on Thursday, will extend beyond the world’s largest economy.

What is happening this week?

The Federal Open Market Committee (FOMC), which sets official US interest rates, meets on Wednesday and Thursday and announces its latest policy decision on Thursday at 7pm UK time (2pm Washington DC time). Minutes from its last meeting in July suggested members were getting ready to hike interest rates for the first time in almost a decade. So-called ‘lift-off’ could perhaps as soon as this September meeting.

Janet Yellen, chair of the US Federal Reserve, or Fed, will give a news conference half an hour after the announcement and investors will be looking to her for clues on future moves from the central bank. Even if the Fed has just hiked, Yellen is expected to take a “dovish” tone, emphasising that any further tightening will be gradual and only happen when economic conditions are right.

How does the central bank influence the economy?

The 12-member FOMC holds eight scheduled meetings a year, around every six weeks, when it decides on key short-term interest rates to meet its economic goals of “maximum employment and stable prices”. When deciding whether to raise these rates the committee will weigh up news from the US labour market, the likely outlook for inflation and developments in the global economy.

The committee sets a target for the Federal Funds rate, a key interest rate between commercial banks which in turn influences borrowing costs throughout the economy. That rate has been held close to zero (technically it is a range of 0.0% to 0.25%) since 2008.

Since 2008 the Fed also sought to buoy the crisis-hit US economy with a vast bond-buying programme. That quantitative easing (QE) scheme involved printing money to buy assets off financial institutions, in the expectation that they would reinvest the funds in the wider economy.

Why are interest rates so low?

Extraordinary times warrant extraordinary monetary policy, is the thinking from the Fed. In its own words: “The financial crisis that began in 2007 was the most intense period of global financial strains since the Great Depression, and it led to a deep and prolonged global economic downturn.”

So why should US rates rise now?

This week marks seven years since the collapse of US bank Lehman Brothers and, on the surface, the world’s biggest economy appears to have put the global financial crisis behind it. In that case, why leave monetary policy on an emergency setting? Unemployment is at 5.1%, the lowest since March 2008. Economic growth has been picking up. GDP rose at a 3.7% seasonally adjusted annual rate in the second quarter of 2015.

Unless these stronger conditions are matched by more normal monetary policy, economists see risks for inflation rising too high in the future. The Fed’s favoured inflation measure, the index of personal consumption expenditures (PCE), is near zero and well below the central bank’s 2% target.

“Inflation is not a problem now, but zero rates are a recipe for excess inflation down the road. The longer the wait, the higher the risks. If inflation does break out, the Fed will be forced to tighten aggressively, causing far more damage to the US and global economy than starting now,” says Deutsche Bank’s chief economist David Folkerts-Landau.

Federal Reserve vice-chairman Stanley Fischer recently said there was “good reason to believe that inflation will move higher as the forces holding down inflation dissipate further”.

There is also an argument that after all the build-up to a potential rate hike this week, pulling the trigger at last would actually remove some of the volatility from financial markets.

“Once the dust has settled, the combination of a small hike and a relatively dovish statement may be better received than yet another delay. The latter might simply be interpreted as a sign that the Fed is more worried about the global economy,” said Julian Jessop, chief global economist at the consultancy CapitalEconomics.

What are the arguments for waiting?

While all may look rosy with the US economy for now, there are a few clouds on the horizon. There have been wild swings on financial markets in recent months and signs that the global economy is losing momentum. The market turmoil stems from China, where an economic downturn has coincided with a stock market rout.

Against the backdrop of waning demand from China, oil prices have fallen sharply, keeping a lid on inflation in the US and elsewhere. Falling oil prices also hurt the economy in the US given its role as an energy producer.

Responding to volatile global markets, Bill Dudley, president of the New York Federal Reserve and a member of the central bank’s rate-setting committee, said in late August that a September interest rate rise was “less compelling” than it had been a few weeks earlier.

What effect would a rate rise have in the US?

Whether the Fed edges interest rates up now or later, the move will be seen as the first in a series of small hikes to gradually take borrowing costs to more normal levels. The central bank’s comments and updated economic forecasts on Thursday will be scrutinised for clues.

The dollar would likely strengthen on the back of higher official rates and yields would rise on US government bonds. The Fed’s move would also be felt throughout the economy as borrowing costs shift higher. That is good news if you are a saver. Not so good if you are in debt.

The prospect of rising rates has already sparked jitters in equity markets and huge movements of capital as investors fear rising costs will affect business borrowing and consumer spending.

— Lawrence H. Summers (@LHSummers)August 24, 2015

No time for an interest rate hike. Read my column: https://t.co/XmY9PS2OO2

There have also been warnings that a hike could cost jobs. Former US Treasury secretary Larry Summers believes higher rates would mean companies sit on their cash rather than investing in new hires or new equipment.

How would a hike be felt outside the US?

The biggest concerns about the non-US effects of a Fed hike centre on emerging markets.

Money had flowed into fast-growing developing countries while interest rates were at rock-bottom levels in advanced economies but the prospect of an imminent US rate hike has seen those funds start to flow back out as investors move their money on the expectation of improving returns. The pressure on Asian emerging markets, where currencies such as the Malaysian ringgit have slumped to their lowest in more than a decade, has been exacerbated by the prospect of China’s malaise spreading to its neighbours.

The Fed would argue, however, that it sets interest rates for the US economy not the rest of the world.

For the eurozone, a hike in the US puts policy there even more at odds with the ultra-loose stance of the European Central Bank, which has embarked on its own QE programme. That will put the single currency under pressure against the dollar.

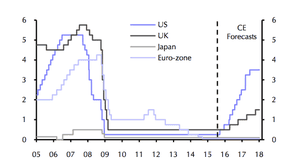

Diverging official rates

In the UK, the Bank of England (BoE) could follow the Fed’s lead and finally hike interest rates after more than six years at a record low of 0.5%. But UK inflation remains well below the BoE’s target and at its last meeting, only one of the nine-member monetary policy committee voted for a rate hike.

Source: https://www.theguardian.com